Future of the Exurbs: Will Prices in Outer Suburbs Stay High—or Fall?

The COVID-19 pandemic turned the real estate market inside out, as the big cities swiftly lost their megawatt appeal—with their home prices and rents plummeting accordingly—while the farthest-out, sleepiest suburbs suddenly became new hot spots for homebuyers.

The exurbs, as these outer suburbs are called, experienced the highest price growth over the past year, according to Realtor.com®. While suburbs closer to the urban core remained the most popular with buyers, exurbs saw the biggest increase in interest from home shoppers.

That surge was driven by the fear of COVID-19, the rise of remote work, and the search for more affordable homes with enough square footage in which to quarantine with the whole family. Builders have also been putting up new homes in these areas, where land is cheaper and more plentiful.

However, the future of the exurbs in a post-pandemic world remains uncertain. Many workers will eventually have to return to their offices, even if it’s just a few days a week, making the issue of a commute relevant once more. Plus, exurbs have historically been more vulnerable to downturns—they were hammered in the Great Recession. Fears of a bubble, however unlikely, could give buyers pause.

These areas could find themselves competing with the appeal of urban life again. Big cities became more attractive as vaccines became available and businesses and entertainment venues reopened their doors.

However, the emergence of the delta variant could complicate things further.

“The jury is still out,” says Realtor.com Chief Economist Danielle Hale. “It’s possible that some areas that saw prices rise because they were particularly attractive during the pandemic might not be able to sustain those high prices. … The factors that drew people to those areas, like having a lot of space and being far away from everything else, may change.”

Will home prices in the exurbs eventually fall?

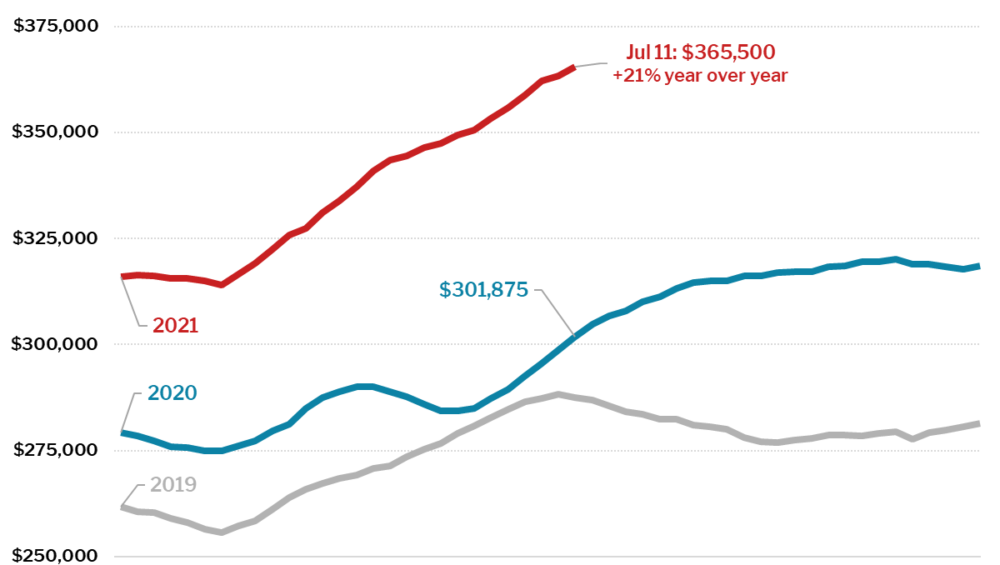

Prices have grown the most in the exurbs during the pandemic. Depicted above are exurban ZIP Codes in the 100 largest metropolitan areas with enough listings to derive meaningful trends. (Sabrina Speianu/Realtor.com)

The big question for many is whether prices in the exurbs will continue to go up—or if they’ll decline. Since buying a home is the largest investment most people will ever make, most buyers want to be as sure as they can that the value of that investment won’t go down.

The shortage of homes for sale and higher prices in the closer-in suburbs and cities may continue to force aspiring homeowners on a budget and struggling renters to move farther out to find more affordable housing. That demand could keep prices in the exurbs from falling.

“The desire for affordability, which is only going to become more important as interest rates go up, is going to keep interest in the suburbs and outer suburbs high. They have always been the escape valve for high city prices,” says Hale.

“It’s not a new phenomenon that, when people can’t afford the city, they look further out,” she continues.

The potential staying power of the work-from-home phenomenon will also likely prevent prices from slipping too much. If workers can go entirely remote or commute only once or twice a week, they may be more likely to seek out cheaper real estate in a more bucolic setting.

“I don’t think prices will drop off dramatically,” says Kelly Mangold, who specializes in real estate economics at the consulting firm RCLCO. “Everyone’s not going back to the office five days a week anytime soon.”

Investors, who typically seek out cheaper housing they can buy and flip or rent out, may also give these areas a boost.

“We’ll still see healthy price appreciation,” says Devyn Bachman, vice president of research at John Burns Real Estate Consulting. Or in certain areas that experienced rapid price hikes, “you may see small corrections in these markets.”

On the flip side, more square footage and larger backyards require more maintenance, and many cash-strapped buyers may not want to pay to have all that grass mowed or the snow shoveled. It’s also more expensive to heat a 3,000-square-foot home than one half the size.

Higher mortgage interest rates could also hurt prices in the exurbs. Rates fell below 3% for an average 30-year fixed-rate mortgage during the pandemic. This made ultrahigh prices more palatable, because the lower rates offset some of the higher costs, helping monthly mortgage payments stay affordable. If rates rise, home prices won’t have the same room to rise. They could even dip in the places that experienced the biggest run-up in prices.

“The mortgage payment becomes very high,” says Ali Wolf, chief economist of building consultancy Zonda. “There are locals who will just get crushed.”

But housing experts don’t expect a full-blown crash even if prices do correct a bit. There is more demand for housing than there are homes available—the opposite of what happened in the mid-2000s. And unlike in the last real estate bubble, only the most qualified borrowers are being approved for mortgages, lessening the chances of another foreclosure crisis.

Builders are putting up more homes in the exurbs

The thing about remote suburbs is that they have potential for development—and builders have taken notice. There’s more land available for building in these areas.

Roughly 9.2% of construction on single-family homes was in the exurbs of large metropolitan areas in the second quarter of 2021, according to the National Association of Home Builders. That’s in addition to the 8.9% of construction in the outer suburbs of medium-sized metropolitan areas.

“Exurbs have great potential for development,” says Realtor.com’s Hale. “They have more open space for builders to build and create things, which is a bit harder to come by the closer in you get to the city.”

Putting up more homes brings in new residents, which attracts more grocery stores, shops, restaurants, and entertainment. These amenities in turn make these communities more desirable and could keep the housing markets in these areas strong, unless the supply of homes outstrips the demand for them.

But overbuilding doesn’t seem too likely. Builders have a lot of catching up to do to meet demand, and they’ve been skittish since the last real estate bust.

“Builders are skeptical about how much this may last and are being more conservative about shifting their pipeline in that direction,” says Hale.

Origination: https://www.realtor.com/news/trends/future-of-the-exurbs-where-prices-jumped-during-pandemic/