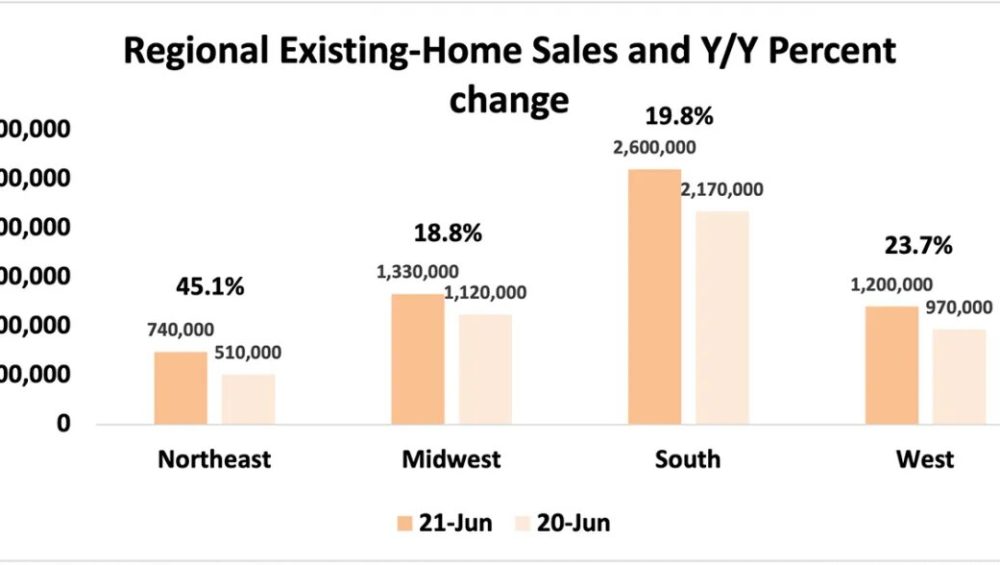

NAR released a summary of existing-home sales data showing that housing market activity this June increased 1.4% from May 2021. June’s existing-home sales reached a 5.86 million seasonally adjusted annual rate, and June’s sales of existing homes increased 22.9% from June 2020.

The national median existing-home price for all housing types rose to $363,300 in June, up 23.4% percent from a year ago. Home prices have continued to rise, and this marks the 112th consecutive month of year-over-year gains.

Regionally, all four regions showed double-digit price growth from a year ago. The Northeast had the largest gain of 23.6% followed by the South with an increase of 21.4 %. The Midwest showed an increase of 18.5% and the West had the smallest price gain of 17.6% from June 2020.

June’s inventory inclined 4.1% from last month, standing at 1.26 million homes for sale and indicating some slight easing of the tight inventory condition.

However, compared with June of 2020, inventory levels are 18.2% lower. This would mark 25 straight months of year-over-year declines. It will take 2.6 months to move the current level of inventory at the current sales pace, well below the desired pace of 6 months.

Demand remains strong as home buyers are snatching listings quickly off the MLS, and it takes approximately 17 days for a home to go from listing to a contract in the current housing market. A year ago, it took 24 days.

From May 2021, all four regions had inclines in sales except the South, where sales were flat. The Midwest had the biggest gain of 3.1% followed by the Northeast with an incline of 2.8%. The West region had the smallest increase in sales of 1.7%.

From a year ago, all four regions showed double-digit inclines in sales. The Northeast region had the largest gain of 45.1% followed by the West with an incline of 23.7%. The South had an increase in sales of 19.8% followed by the Midwest with the smallest gain of 18.8%.

The South led all regions in percentage of national sales, accounting for 44.3% of the total, while the Northeast had the smallest share at 12.6%.

In June, single-family sales increased 1.4% and condominiums sales were up 1.4 compared to last month. Single-family home sales were up 19.3% while condominium sales were up 56.5% compared to a year ago, reflecting the impact of the pandemic lockdown. The median sales price of single-family homes rose to 24.4% at $370,600 from June 2020, while the median sales price of condominiums rose 19.1% at $311,600.

You are in your new home by now, what an exciting day! After the whole hunting process, filing the papers, your dream home is yours. However, you see yourself surrounded by piles of boxes, so the question now is, what do you unpack first?

After that, so many questions come up: Where are the kitchen supplies? Where are the towels? Where is the dog’s food? We know that organizing a house can be exhausting, but today we are going to give tips on how to put away everything efficiently, and how to make this process as quick and smooth as possible.

First things first

To start, it is essential that you prepare the house for the arrival of your stuff.

Clean and prepare your house

It is way easier to clean up the shelves, vacuum, and mop when you don’t have furniture inside. However, if you don’t get to your new place early enough to do the cleaning, hiring a professional to do the job is always a good option.

Inspect and organize your belongings

Check all the delivered boxes and the inventory sheet to make sure everything arrived in your new home and nothing is missing. After that, place the boxes in each room that the items belong to so that it will be easier to find things in the house.

Set up larger furniture and appliances

Setting up the major furniture, like the bed, dresser, dining table, etc., will make it easier to put all the small things in the right place. Have your interior design already planned so that you don’t need to move the heavy pieces after setting up.

Tend to the necessities

Kitchen

The kitchen might take a while to finish due to the number of pieces it has. However, it is the first place you should start unpacking because of the cold food in the refrigerator and, of course, no one wants to be hungry during the organization.

Bathroom

Another area that is fundamental is the bathroom. For sure, after a whole day of unpacking, you will want to wash away the weariness and the stress of moving, so having everything within reach is the best option. Therefore, you should unpack the toiletries, like soap, toothbrushes, toothpaste, shampoos, and conditioners. After that, put away all the towels and rags.

Bedding

A long day of moving needs good rest. You won’t be able to unpack the whole bedroom, but the bedsheets, pillow, and blankets are the most important now. Remember to get the curtains up, as well, so that you will keep your privacy and will not wake up with the sun in your face. The rest of the stuff can wait until the next day.

Kids and pets

Unpack what they are going to need for the day, for example, diapers, bath supplies, and clothes for the night. For the pets, have their bed, food, and medicine ready for when they need it.

Keep in mind that you are going to be unpacking for a while. It may take a week or so, but now you know what is more important to organize when you first arrive at your new home. Just keep going until you have finished everything, and don’t freak out with the stress of moving, try to have fun, put on some music, and this can be fun as well!

National property broker Redfin is reporting that nearly one-third (30%) of U.S. home purchases this year were paid for with all cash.

That’s up from 25.3% during all of 2020 and represents the largest share since 2014, when 30.6% of homes were purchased with all cash. Redfin analyzed county records published from January 2021 to April 2021.

Cash purchases are on the rise as Americans reap the benefits of a strong stock market. The S&P 500 Index has gained 36% in the past 12 months alone, as of July 14, 2021.

“I’ve never seen more cash in Boise’s housing market than I’ve seen in the past year,” said Shauna Pendleton, a Redfin real estate agent in Idaho. “I just sold a $700,000 home to a cash buyer last week. The entire $700,000 came from his E*Trade account.”

Additionally, remote work has allowed homeowners in expensive cities, including San Francisco and New York, to sell their homes and move to less expensive areas, where they can often afford to buy properties in cash.

“Affluent homeowners in Seattle, Portland, and parts of California are selling their homes for $1 million or $2 million,” Pendleton said. “Then they’re coming to Boise, where they’re buying houses that are twice the size for half the price.”

Investors, who often pay in cash, are wading back into the housing market after pressing pause at the onset of the pandemic. U.S. home purchases by investors rose 2.7% year over year in the first quarter, marking the first period of growth since the coronavirus pandemic began.

The rise in all-cash home purchases is posing challenges for many first-time and lower-income homebuyers, who are having trouble competing with cash offers. While competition is easing slightly, about two-thirds of the home offers written by Redfin agents still face bidding wars.

In Parts of Florida, More Than Half of Homes That Have Sold This Year Were Bought With Cash

In the West Palm Beach, FL metro area, 52.6% of home purchases this year were paid for with all cash. That’s the largest share of the 86 metropolitan areas in Redfin’s analysis. Metros must have had at least 3,000 recorded home sales from Jan. 1, 2021, and April 30, 2021, to be included in this report. West Palm Beach was followed by Naples, FL (52.5%), Nassau County, NY (50.2%), North Port, FL (49.4%), Port St. Lucie, FL (46.2%), Greenville, SC (45.4%), Palm Bay, FL (44.1%), Cape Coral, FL (44.1%), Des Moines, IA (41%) and Jacksonville, FL (40.1%).

“Florida is a big second-home market, and second-home buyers often pay with cash,” said Dina Blau, a Redfin real estate agent in the West Palm Beach area. “During the pandemic, folks also flocked to Florida to buy primary homes. They sold their houses in New York, New Jersey, Chicago, or California and used the proceeds to pay cash for properties in Florida.”

California Has Lowest Share of Cash Transactions

Expensive California metros, where it’s more challenging to pay with cash because home prices are relatively high, were at the bottom of the list. In both San Jose, CA and Oakland, CA, 12.5% of reported home purchases this year used all cash–the lowest share of the metros Redfin analyzed. Next came Richmond, VA (16%), Los Angeles (16%), San Diego (16.2%), Lake County, IL (17.2%), Sacramento (17.7%), San Francisco (17.8%), Oxnard, CA (18%) and Bakersfield, CA (19.3%).

Still, buyers in California aren’t out of the woods, according to Steven Moore, a Redfin real estate agent in Los Angeles.

“I recently put in a $1.8 million offer on a home that was listed at $1.7 million,” Moore said. “The top 10 offers–out of 40 total–all came in at around $2 million and were all cash.”

Over 4% of homes for sale had price drops, and pending sales are down more than 10% from their 2021 peak.

The average weekly share of homes for sale with a price drop passed 4% for the first time since September, another signal that the hyper-competitive housing market is cooling. Other indicators corroborate the slowdown: the share of homes sold over list price, the share of homes sold within a week and median days on market are all also either cooling off or plateauing.

Pending sales were up 11% from a year ago, but down 11% from the 2021 peak, and asking prices have been relatively flat since late May. Even amid this shift, sellers remain in the driver’s seat, as home prices continued to rise more than 20% from a year ago and the number of homes for sale sits 30% below the same time last year.

Looking ahead, some indicators of early-stage homebuyer interest like tour activity, mortgage purchase applications and requests for service from Redfin agents have shown signs of picking back up. It’s too early to call it a trend, but we’ll continue to track whether this continues and leads to sales and competition heating back up.

Unless otherwise noted, the data in this report covers the four-week period ending July 11. Redfin’s housing market data goes back through 2012.

“Asking prices are still high, but the share of listings with price drops is rising steadily and could soon reach pre-pandemic levels,” said Redfin Chief Economist Daryl Fairweather. “That’s an early indication that we are past the peak for this intense seller’s market. Buyers may begin to regain some negotiating power on properties that have been on the market for more than a week.”

Key housing market takeaways for 400+ U.S. metro areas:

Data based on homes listed and/or sold during the period:

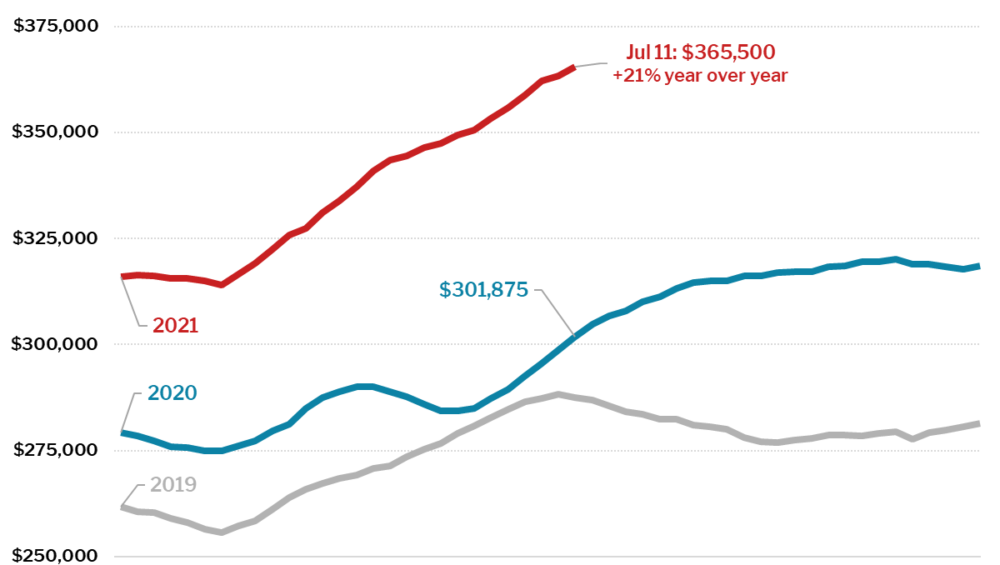

The median home-sale price increased 21% year over year to $365,500, a record high.

Asking prices of newly listed homes were up 12% from the same time a year ago to a median of $361,700. This is up 0.5% from the four-week period ending July 4, but down 0.6% from the all-time high two weeks ago.

Pending home sales were up 11% year over year, the smallest increase since the four-week period ending July 5, 2020. Pending sales were down 11% from their 2021 peak during the four-week period ending May 30, compared to a 4% decrease over the same period in 2019.

New listings of homes for sale were up 3% from a year earlier. The number of homes being listed is in a typical seasonal decline, down 8% from the 2021 peak during the four-week period ending May 23, compared to an 11% decline over the same period in 2019.

Active listings (the number of homes listed for sale at any point during the period) fell 30% from 2020—the smallest decline since the four-week period ending January 31—and have climbed 9% since their 2021 low during the four week period ending March 7.

53% of homes that went under contract had an accepted offer within the first two weeks on the market, well above the 44% rate during the same period a year ago, but down 4.2 percentage points from the high point of the year, set during the four-week period ending March 28.

38% of homes that went under contract had an accepted offer within one week of hitting the market, up from 32% during the same period a year earlier, but down 5.1 percentage points from the high point of the year, set during the four-week period ending March 28.

Homes that sold were on the market for a median of 15 days, an all-time low that has been flat for the last four weeks, and down from 38 days a year earlier.

A record 55% of homes sold above list price, up from 28% a year earlier. This measure is plateauing, having been 54-55% since the four-week period ending June 27.

The share of homes for sale with price drops rose to 4.1%, continuing to surpass 2020 level, and climbing closer to 2019 levels (4.7% at this time in 2019).

The average sale-to-list price ratio, which measures how close homes are selling to their asking prices, increased to 102.3%. In other words, the average home sold for 2.3% above its asking price. This measure is an all-time high and 3.5 percentage points higher than a year earlier, but growth has slowed and it may be at or near its peak for the year.

Other leading indicators of homebuying activity:

Mortgage purchase applications increased 8% week over week (seasonally adjusted) during the week ending July 9. For the week ending July 15 30-year mortgage rates fell to 2.88%, the lowest level since mid-February.

From January 1 to July 11, home tours went up 23%, compared to a 50% increase over the same period last year according to home tour technology company ShowingTime.

The seasonally adjusted Redfin Homebuyer Demand Index—a measure of requests for home tours and other services from Redfin agents—rose sharply during the week ending July 11, and is currently up 15% from a year earlier.

Refer to our metrics definition page for explanations of all the metrics used in this report.

Finding the perfect home is a challenge. Some homebuyers have their preferences when it comes to suburbs or cities, quiet neighborhoods, or busy one. Today, we are going over the pros and cons of purchasing a house close to a school. If you have kids at school or college-aged, this is for you!

Pros

Affordability

Many neighborhoods that have schools nearby have low-cost properties. This is because a lot of them are rented by students who can’t afford something expensive. This results in the value of the houses not being so high, so if you are looking for something more affordable, this could work for you.

Playground Nearby

This is a huge advantage for parents that have young kids. You are not going to need to pack a car to go to a park, as it is walking distance to your home. Some of them have fences, which allow kids to stay safely by themselves, and they may even have basketball courts and other amenities.

May Increase Property Value

Houses near a school — especially a good school — have increased value due to demand from parents that want to live closely. Many of them are willing to pay more for a property that is close to a prestigious school. Homebuyers might have to increase their budget by 10 – 20% to live in these places, so it is important for sellers to know this.

Kids can walk to school

The good news here is that parents who live close to their child’s school can avoid the pick-up/drop-off lines. Another good point is kids can exercise by walking to school, the parents will save money with bus passes, and they won’t need to wake up so early.

Cons

Increased Traffic

During the hours for drop-off and pick-up, the traffic could be heavy in the area. Additionally, if the school is really big, it can change the quality of the air and increase pollution. There may be some parking inconveniences as well.

Noisy Neighborhood

A place near a school will have many kids playing together and will be very noisy. For those who like a quiet and peaceful area, this may not be for you. Usually, the sounds cease after school ends, but these places generally have many extra-curricular activities for the kids after school.

May Be Harder to Sell

Some homebuyers don’t consider buying homes close to schools, even if they are good properties. Another point is that the value of the house can change depending on how good the school is, and a school can either increase or decrease the value of your property, depending on its reputation.

These are the pros and cons of living near a school. Now you have the know-how to choose what fits best for you and your family!

The penthouse on top of one of New York City’s oldest skyscrapers has become available. Located in a historic Lower Manhattan building, the unit is available for $2 million.

Billed as one of New York City’s “crown jewels,” the full-floor penthouse in the landmarked Liberty Tower offers an unusual aerie, where the owner is at eye level with the ornamental decorations that adorn the exterior.

Upon its completion in 1979, the notable building was “one of only a handful of skyscrapers,” according to the New York Times. “Its striking Gothic style, the centuries-old inspiration for cathedral spires that reach into the sky to approach the divine, is central to the tower’s romantic appeal.”

Living room (Brown Harris Stevens)Dining room (Brown Harris Stevens)Sloped ceiling (Brown Harris Stevens)Bedroom (Brown Harris Stevens)Bathroom (Brown Harris Stevens)Views with building ornaments (Brown Harris Stevens)

Now known as Liberty Tower, the Gothic Revival-style building designed by Henry Ives Cobb initially opened as office space. The law office of Franklin D. Roosevelt was one of the first tenants of the 33-floor tower in 1910. (FDR later served as president, from 1933 to 1945.)

Soon after World War I, Sinclair Oil acquired the building, and in 1979, the structure was converted into residential apartments.

Unlike many sleek monoliths of the modern era, this historic tower, with its terra-cotta facade and ornate design, has more of a Notre Dame Cathedral vibe than a typical New York City skyscraper. The exterior is decorated with birds, alligators, flowers, and gargoyles.

Designated a city landmark in 1982 and added the following year to the National Register of Historic Places, the building also received a preservation award from the New York Landmarks Conservancy in 2010.

Last sold in 2005 for $958,000, the apartment could bring quite a windfall if it sells close to its asking price. Still, as penthouses in Manhattan go, the price could be considered a relative deal. Especially from that perch overlooking the city.

“Views of the Hudson and East rivers and the Wall Street Canyon are spectacular,” says the listing agent, Richard N. Rothbloom with Brown Harris Stevens. “And at eye level, right outside each window, are large sculptures of falcons, lions, and fleurs-de-lis that decorate the top of the building.”

The top-floor unit, with two bedrooms and two bathrooms, spans the entire 32nd floor, a total of 1,700 square feet. The living space boasts a dozen windows with southern, western, and eastern exposures, under 11-foot vaulted ceilings in rooms that have the “dramatic slopes of a garret,” as the listing description puts it.

And we know why. Rothbloom notes that the top floor was “formerly the attic of landmark Liberty Tower.” That’s one fancy crawl space!

The foyer opens onto an expansive living room, featuring a wood-burning fireplace, nooks, office, and home theater. The kitchen looks out to a dining room, which can serve both for daily meals and to hold formal gatherings.

The primary bedroom includes a closet system and a double-vanity bathroom with a combination tub and shower.

A second bedroom, currently used as a library, also comes with a bathroom with a glass-enclosed shower.

Other details include hardwood and marble flooring that runs throughout the home. The space also features a central HVAC system, as well as a washer and dryer.

The pet-friendly building is staffed with 24-hour door attendants, porters, and a live-in superintendent.

The location is convenient to dining and shopping at the Oculus, Eataly, and the redesigned South Street Seaport.

For those with offices in the Financial District, that’s in the neighborhood, too. Subway lines converge at Fulton Center, and there’s also quick access to Citi Bike, and the PATH train at the World Trade Center station.

Considering moving to Philadelphia? Before you start apartment hunting, learn about the local rental market. Make sure you know the average rent in Philadelphia to get your budget started!

Average Rent in Philadelphia

The average rent for a Philadelphia studio apartment is $1,415

The average rent for a Philadelphia 1-bedroom apartment is $1,721

The average rent for a Philadelphia 2-bedroom apartment is $2,042

The average rent for a Philadelphia 3-bedroom apartment is $2,059

Interested in starting your Philadelphia apartment search, here’s how to find an apartment in Philadelphia.

Philadelphia Rent Trends: Rent Growth

Philadelphia rents have increased by 1.26% compared to last month, and are up by 2.83% compared to last year.

For a broader discussion of rent changes across the country, check out our National Rent Report. You can download the raw data containing rent estimates for hundreds of cities across the country.

Philadelphia Rent Trends: Inventory by Average Apartment Rent

19% of apartments in Philadelphia are studio apartments.

42% of apartments in Philadelphia are 1-bedroom apartments.

25% of apartments in Philadelphia are 2-bedroom apartments.

14% of apartments in Philadelphia are 3-bedroom apartments.

Average Rent in Philadelphia Neighborhoods

Has your ideal Philadelphia neighborhood already been picked out? Rent prices across neighborhoods can vary, so get familiar with the average rent prices across the various neighborhoods in Philadelphia.

The most expensive neighborhoods in Philadelphia are University City ($2,487), Center City West ($2,204), and Rittenhouse Square ($2,086).

The most affordable neighborhoods in Philadelphia are Washington Square West ($1,489), Brewerytown ($1,484), and Harrowgate ($1,246).

What Salary Do You Need to Live in Philadelphia?

Using the 30% rule, we can give a rough estimate of the salary needed to rent an apartment in Philadelphia. If these numbers look high, remember that a roommate or two can drastically cut down your monthly rent!

If you are renting an average-priced studio apartment in Philadelphia, your annual salary should be around $50,940 or higher.

If you are renting an average-priced 1-bedroom apartment in Philadelphia, your annual salary should be around $61,956 or higher.

If you are renting an average-priced 2-bedroom apartment in Philadelphia, your annual salary should be around $73,512 or higher.

If you are renting an average-priced 3-bedroom apartment in Philadelphia, your annual salary should be around $74,124 or higher.

If you’re considering renting in Philadelphia, be sure to learn more about the cost of living in Philadelphia.

Having trouble deciding how much rent you can afford? Try using a rent calculator.

Mortgage demand fell for the second week in a row, as low inventory and high home prices continue to weigh on the housing market.

Mortgage applications decreased 1.8% last week, according to the Mortgage Bankers Association’s seasonally adjusted index, falling to the lowest level since the beginning of 2020, before the coronavirus pandemic started to take a toll on the economy.

Both refinance and purchase applications took a hit, even as mortgage rates slipped.

Mortgage applications to refinance a home dropped 2% for the week and were 8% lower than a year ago. Refinance applications have trended lower than 2020 levels for the past four months, according to the MBA.

Home purchase applications dropped 1% for the week and came in 14% lower than a year ago.

“Swift home-price growth across much of the country, driven by insufficient housing supply, is weighing on the purchase market and is pushing average loan amounts higher,” said Joel Kan, MBA’s associate vice president of economic and industry forecasting.

Falling mortgage rates didn’t spur demand. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($548,250 or less) dropped 5 basis points to 3.15, with points decreasing to 0.38 from 0.39 (including the origination fee) for loans with a 20% down payment.

Mortgage rates loosely follow the yield of the 10-year Treasury. Mortgage rates dipped despite good economic news, Kan added.

“Treasury yields have been volatile despite mostly positive economic news, including last week’s June jobs report, which showed ongoing improvements in the labor market. However, rates continued to move lower – especially late in the week,” he said. “The 30-year fixed rate was 11 basis points lower than the same week a year ago, but many borrowers previously refinanced at even lower rates.”

New York State Governor Andrew M Cuomo has launched a $9 million fund to support research into ways of capturing atmospheric carbon and turning it into useful products.

The Carbontech Entrepreneurial Fellowship Program will provide technical expertise for “carbon-to-value” technology that stores captured CO2 in physical objects.

The programme is part of the state’s aim of becoming a leading hub for carbontech businesses as well as supporting its goal of reducing its greenhouse gas emissions by 85 per cent by 2050.

“Revolutionizing the development of products made from carbon capture will create the landscape to achieve deep decarbonization in our fight against climate change,” Cuomo said.

“Attracting scientists with cutting-edge skills and knowledge to realize new products is essential to growing our green economy, and we are bringing their research out of the lab to pave the way for a more climate-resilient future to benefit all New Yorkers.”

Programme commercializes removal of CO2

The programme is part of a burgeoning “carbontech” sector that aims to commercialize the removal of atmospheric CO2, which is the main cause of climate change.

Players include Finnish company Solar Foods, which plans to make food from captured carbon, and Australian company Mineral Carbonation International, which turns CO2 into construction materials.

Other carbontech companies include Canadian company Carbicrete, which makes concrete from CO2, and Dutch brand Made of Air, which makes bioplastic from carbon-rich farm and forest waste.

Carbon capture key technology in the fight against climate change

The Carbontech Entrepreneurial Fellowship Program will be administered and funded by the New York State Energy Research and Development Authority (NYSERDA).

“By focusing on bringing together novel ideas with entrepreneurs, we are fostering a new pipeline of sustainable, emission-reducing products that will help New York shrink its carbon footprint and build healthier communities,” said NYSERDA President and CEO Doreen M Harris.

“Carbon-to-value” is a similar concept to carbon capture and utilization (CCU), which is emerging as one of the key planks in the fight against climate change. It involves capturing carbon from the atmosphere and turning it into useful objects that double as long-term stores for the element.

Atmospheric carbon can be captured using direct air capture machines, such as those developed by Climeworks. It can also be captured naturally in biomass including trees, hemp, bamboo and algae.

Earlier this year Elon Musk launched the $100 million XPrize Carbon Removal competition, which calls for new devices that sequester carbon dioxide.

“Decarbonization a top priority”

The New York State fellowship programme follows April’s launch of the $10 million Carbontech Development Initiative, a programme “to establish New York State as a world-class hub of carbon-to-value research, technology transfer and commercialization.”

“Capturing carbon and using it requires innovation, and this program will enable us to work with industry leaders who possess the necessary knowledge, technology, and vision,” said Cuomo in April.

“If we want to reach our ambitious goal of creating a greener, cleaner future for all New Yorkers, we need to make decarbonization a top priority. The Carbontech Development Initiative will help us to establish this innovative practice right here in New York, while simultaneously fueling economic growth and community engagement.”

New York City’s greenhouse gas emissions were visualized in a groundbreaking animation by graphics firm Real World Visuals.

Released in 2012, the computer-generated timelapse shows the city being buried under a mountain of bubbles representing the city’s 54 million tonnes of annual CO2 emissions.

While there has been uncertainty around the future of office real estate as a result of the pandemic, the asset class is performing better than some have expected. As the vaccine continues to become more widely distributed, utilization rates in office space continue to steadily increase. More than 95 percent of employers are anticipating a nearly full-return to office, which is significant considering occupancy was less than 50 percent in June of 2020. Life science and medical office space in particular, which provide the most stability during times of economic downturn, have been helping to bolster office performance. IIn this article we will cover:

The office industry and the case for investment in this asset class

The progression of modern office space

Life sciences and the impact Covid-19 has had on the industry

The evolution of the life science industry since the early 2000s

The future of office and the life science industries

COUNTERINTUITIVE: WHY YOU SHOULD INVEST IN OFFICE RIGHT NOW

During the pandemic, companies around the world had to switch from collaborative office environments to remote working. An estimated 62(1)percent of employed Americans worked at home during the crisis, compared to 31 percent prior to the pandemic. The resulting rise in U.S. office vacancy rates and the declining average gross asking rent caused concern for the future of office real estate.

According to CoStar, office-using employment fell 7.8 percent from February to April of 2020, but then increased by about 5.5 percent during the summer. The result was that office-using employment was only down about 2.8 percent from the February peak. Despite widespread fear of vacant offices, as of Q2 2021, the office vacancy rate exceeded 12%, up 2% year-over-year.

The reality is that while there has certainly been an impact on occupancy, the office sector is not only a safe bet, but continues to be a strong investment option. It is predicted that employees will be returning to office space earlier than anticipated. During his discussion with Willy Walker in Q4 2020, Owen Thomas, CEO and Director of Boston Properties, predicted that occupancy of his own buildings could be up to 20 percent by the end of the first quarter 2021, 50 percent by Labor Day, and up to 75 percent by the end of the third quarter.

Additionally, niche office sectors, such as life science and medical office which remain stable even during economic downturns, have bolstered the office market’s strength.

EVOLUTION OF OFFICE SPACE: NEW OPPORTUNITIES

Studies have shown that employees are eager to return to the office, but changes will need to be made to accommodate the evolving needs of tenants. According to a survey conducted by Deloitte, 68% of employers plan to implement some type of hybrid workplace model in 2021, while only 1% will remain fully virtual. With hybrid work schedules and increased flexibility, there will need to be more incentive for employees to make the trek into the office.

Additionally, the role of office space is shifting toward community and collaboration. Employees will re-enter the office as a means to build personal and professional relationships and connect with the culture, purpose, and mission that the company has to offer.

Investors and developers have an opportunity to reposition office space and gravitate toward a space that reflects the needs of the future. Physical and virtual experiences must be fully integrated into office space to ensure connectivity among all employees. Just as new technology must be integrated into the office space, companies need to invest in home tools and resources so that collaboration is seamless regardless of physical or virtual presence.

93% of people believe that a sense of belonging drives organizational performance (Deloitte 2020 Human Capital Trends). The future of office space will require a design that encourages reconnection, community, and inclusivity. The most successful office spaces will be ones that fully embrace the collaborative environment that corporate America is gravitating toward.

LIFE SCIENCE

COVID-19 ’S IMPACT ON THE LIFE SCIENCE INDUSTRY

Life Science companies are now at the forefront of public interest because of Covid-19 and the rush to develop a vaccine. As the life science industry continues to display remarkable resilience amid the economic downturn, investors and developers have a heightened interest in the space. As a result, institutional investment in the space has been growing at 15 percent per year, totaling more than $6 billion in 2020.

The need for more life science space also creates the need for new construction, as not all office buildings are capable of housing life science tenants due to the demanding lab requirements including high floor loads to handle equipment, proper ventilation, and safety infrastructure.

Buildings are constructed for a specific use, and traditional office structures have a predetermined capacity of weight the building can withstand. While traditional office spaces tend to use lighter materials and can therefore easily accommodate a variety of tenants, life science lab materials include heavy equipment, specific electrical wiring, complex systems, and more. If a building can structurally withstand the load bearing requirements, they can potentially redevelop space to fit a life science tenant’s needs. Still, significant capital expenditures would also need to be invested. If the life science company requires a more traditional or medical office space, such improvements are easier to accommodate.

Although it may seem as though investors and developers are now hopping on a hot trend, the life science industry has been experiencing exponential growth since the early 2000s.

LIFE SCIENCES SINCE THE EARLY 2000’S

An emphasis on individualized and preventative treatment has been a powerful driver of the life science industry for nearly two decades. The sector has also benefitted from technological advances in medicine, changes in healthcare delivery mechanisms, and an aging population. As this demand has grown, so has employment. Since the end of 2013, the number of life science jobs has increased by 70,000 jobs per year.

Life science tenants have proven to be resilient. Even during both economic downturns since 2000, life science industry employment has continued to increase. The powerful drivers of life science industry growth support lab space even during a recession. A high importance is being placed on life science employees, as their average salary has experienced more than 19 percent growth in the last five years. In this same time span, the total number of life science institutions has increased by more than 13 percent, further solidifying the industry’s value (1).

OUTLOOK ON LIFE SCIENCE

The world population continues to grow and age, and there is no shortage of diseases that plague the human population. As the need for treatment, cures, and innovations continues to grow, venture capital investment in the space will continue to increase as well. Investment from government grants and large pharmaceutical companies will also help stimulate the sector and stabilize it during turbulent cycles.

Since custom buildout for life science space requires significant capital, landlords can command higher rents compared to traditional office. As a result, there are high barriers to entry within the life science market. The recent modernization of zoning regulations throughout the U.S. have led to an increase in life science developments. From 2009 to the end of 2019, the amount of lab space in the United States grew from 17 million to 29 million square feet (1). To put that in perspective, the New York office market alone contains 1.4 million square feet.

There is a high demand from institutional capital looking to get into these high-demand markets. From a capital perspective, there will continue to be a massive flight of investment capital from real estate ownership to invest and own properties in the space.

Life science industry growth is aligned with global healthcare expenditures which are expected to rise at a rate of 5.4 percent annually, from $7.7 trillion in 2017 to an anticipated $10.1 trillion by 2022 (2). Additionally, revenue in the industry has been growing at a steady pace throughout the past decade.

Based on the trajectory that the life science industry has had since the early 2000s, along with the newfound recognition of its true necessity post Covid-19, industry growth is expected. Consult with our New York Capital Markets experts for your life science or office industry questions or transaction needs.